| And Then There Is Disaster C |

| By John Mauldin |

Published

08/13/2012

|

Stocks , Options , Futures , Currency

|

Unrated

|

|

|

|

And Then There Is Disaster C

I have contended for some time that Europe is faced with two choices: Disaster A, which is the break-up of the eurozone, or Disaster B, which is the creation of a fiscal union, which keeps the euro more or less intact. Over the last few months I have come to realize that there is indeed a third option, which now looks increasingly possible. This is rather sad, as the third option is just an even worse Disaster C. Each choice carries with it its own unique set of problems, but the outcome of any of the choices will be that the people of Europe face a serious recession, if not a depression. This will impact global growth for more than a short time and, depending on the choice, could plunge the world into a crisis as bad as or worse than the recent credit crisis. In today’s letter we look at all three choices, meanwhile musing on how we arrived at the bottom of such a deep hole, shovels flailing.

Breaking Up Is Hard to Do

“Breaking Up is Hard to Do” was written and sung by Neil Sedaka. It was a #1 hit exactly 50 years ago this week. And while that song was written for a different era, it could be the theme song for much of Europe today.

“Don't say that this is the end. Instead of breaking up, I wish that we were making up again.”

And indeed Europe is quite the dysfunctional family, seemingly always on the verge of breaking up, but somehow managing to patch up the differences. We all have a family member (or two or three) who cause that sort of trouble. We watch the incessant squabbling with unease, wishing they would just settle things and move on. They never deal with the real issues, as that would mean facing too much personal angst and maybe even lead to an admission that the problem is not just with the other party. The euphoria of the initial relationship has been lost in the reality of day-to-day existence. Now, they either sort it out or break up.

These sorts of relationships devolve into co-dependency, where no one is happy. And the rest of us are liable to get sucked in. Even though it’s uncomfortable to be around these people, we still have to interact. But don’t you wish they would get some serious therapy?

And Europe was again acting out this week. First, Italian Prime Minister Mario Monti gave an interview to Der Spiegel, in which he warned of the disintegration of Europe if the European Union allows the euro to fail: “The tension which sprang up in the eurozone in recent years is beginning to look like Europe’s psychological disintegration.”

Remember, Monti was a compromise prime minister, brought in by a parliament wracked by chaos, in the wake of Berlusconi’s withdrawal. But alas, the latter party refuses to slink off quietly into the night with his billions and personal peccadilloes. Monti was appointed rather than elected and is a “technocrat” prime minister. Given the nature of Italian politics, he has done about as well as could be expected. He has an outstanding resumé and is part of the Europhile elite that defends the vision of a united Europe.

The interview itself was mostly the standard-issue political noise emitted from European centers of power. It would have gone unnoticed except for one little item. The Italian prime minister suggested that the heads of the EU national governments make decisions independently from their countries’ parliaments.

“If the governments are tied by their parliaments’ decisions, the lack of freedom of action will result in Europe’s breakdown, rather than deeper integration …”

Was the prime minister not listening to what he was saying? Let me paraphrase for him: “How can we keep the euro together if we have to listen to those pesky parliaments, elected by actual voters?” And he says this prior to the German Constitutional Court ruling on September 12, when most of the German leadership is treading lightly, assuming a “positive” outcome but knowing that nothing is certain? And he does this in one of Germany’s leading publications? Maybe there’s a reason he has never actually run for office. This bonehead statement must have chagrined even his most ardent supporters.

It certainly brought quick responses all over Europe, and especially in Germany.

“German politicians from across the spectrum have reacted furiously to warnings by Italy’s Mario Monti that Bundestag control over EU debt policies threatens to bring about the ‘disintegration’ of the European project. ‘We must make it clear to Mr. Monti that we Germans will not shut down our democracy to pay Italian debts,’ said Alexander Dobrindt, secretary-general of Bavaria’s Social Christians (CSU).” (Ambrose Evans-Pritchard, the Telegraph)

In the time-honored tradition of political spin and “clarification,” Mario Monti almost immediately went back before the press to insist that the words he spoke were not the ones he meant.

The Italian paper Il Libero ran a front-page photo of Angela Merkel, under the headline “The Fourth Reich.” And it gets a lot worse if you start looking.

But just to show off my own ecumenical nature, let me point out that German leaders have their own set of issues. Mainly, they simply have not told the German people what the costs of staying in the eurozone or leaving it are.

In past weeks we have looked at the two major options Europe faces. Let’s call them Disaster A and Disaster B. Disaster A ensues if they decide on a close fiscal union, which will entail giving up substantial national sovereignty (although it will not be sold that way to the voters). It would also mean that the northern states (Germany, the Netherlands, et al.) would have to shoulder large tax burdens in order to share with their southern neighbors and pay for the massive debts they have run up.

Of course, Germany helped create the problem, with its Landesbanks enthusiastically financing the various and sundry debt issues of the peripheral governments and their citizens. Note that when the German government revoked its guarantee of the Landesbanks (regional banks), their cost of borrowing rose significantly. The banks began to “reach for yield,” buying not only US subprime debt (which bankrupted a few of them) but also huge amounts of peripheral European sovereign debt.

The entire Greek bailout was really about using “European” taxpayer money to pay off German and French bank debts. Ditto for the other early bailouts. Now we are down to saving the euro (with the Spanish bailouts), which is an even more costly proposition.

Sidebar: ECB President Draghi famously remarked a week ago that he was prepared to do “whatever it takes” to save the euro, a message that was echoed by Merkel, Monti, and Hollande over the next few days. Then we found out, a week later, that “whatever” did not include using EFSF money to buy Spanish bonds (at least for now and until the German Constitutional Court ruling on September 12). Care to place a bet on what happens after that ruling? I bet there will be a compromise of some sort, to allow the EFSF or the ECB to fund. Draghi did say, after all, that he was simply waiting for a formal request before committing funds. And Spanish PM Rajoy is waiting until September 12, as well, perhaps because he wants to find out exactly what he will be agreeing to if he asks for help.

There is an unwritten rule in legal and political proceedings: never ask a question if you don’t already know the answer. If Spain asks for a bailout and then, for whatever political reason, cannot actually abide by the austerity rules, then that would be worse than not asking.

But it is not just northern (German) taxpayers who will be hurt. Southern-tier countries will have to endure serious austerity measures in order to get the money, which will mean even higher unemployment and deeper recessions – if not depressions. There is no free lunch.

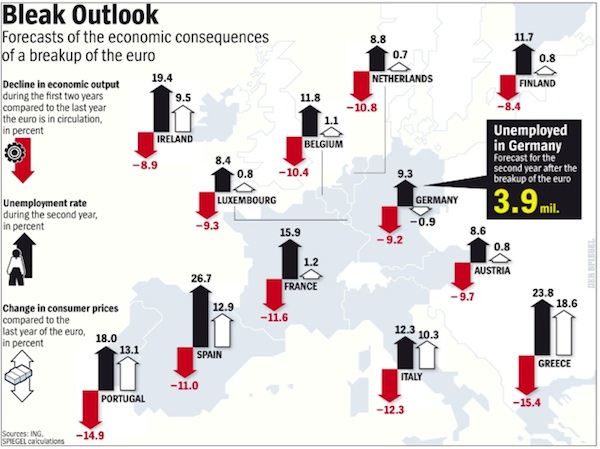

And then there’s Disaster B: the break-up of the eurozone, one way or another. Maine fishing buddy Josh Rosner included this graphic from Der Spiegel in a very impressive report he sent me on the cost to Germany of either leaving or staying in the euro (and which I posted here for Over My Shoulder subscribers). He demonstrates that it is actually much more costly for Germany to leave the euro. He also agrees with me that German leaders are not telling their people what the costs of either option are.

Note that no country does well in a break-up. But the outcomes vary, as some see serious inflation and others see deflation, while all see unemployment rise significantly.

I also note that 56% of Germans want their government to “do everything” to save the euro, with 76% saying a euro break-up would be bad for Germany. In addition, 64% of Germans believe the euro will survive, though 84% think the crisis will worsen, and 56% worry that the economy will deteriorate next year. Finally, 70% believe Merkel is doing a good job. (Source: Bloomberg, reporting on an ARD TV poll)

And Then There Is Disaster C

There is yet a third option that may be turning into the choice du jour. And that is, rather than opting in a straightforward manner for either fiscal union and a eurozone-wide backing of banks, etc., or a break-up of some sort, European leaders might do nothing more than deal with the problem immediately in front of them, moving from crisis to crisis in a slow-motion drift toward fiscal union.

To detail what a real fiscal union would mean and cost, you end up having to ask voters to approve something, and European leaders just don’t know what they will say. What if they say no, nein, non, não, ochi, nee, neen, cha toigh leam, or ei? There are so many ways to say “no” in Europe.

Which is why Mr. Monti is frustrated with the whole parliamentary process of dealing with the euro crisis. It all gets so very messy when you have to explain to voters exactly why and how much they should pay for your personal vision of their future. “If the governments are tied by their parliaments’ decisions, the lack of freedom of action will result in Europe’s breakdown, rather than deeper integration.” This is not unlike someone telling a Russian president to be patient because he will have more flexibility after the election. Just saying.

Who Do You Trust?

The European Union is a rather odd creature. It has a parliament that is widely seen as a joke, with the real work being done by various commissions appointed by national leaders and perhaps ratified by the EU parliament. From my reading, most Europeans are anti-Brussels as opposed to anti-euro. They see Brussels as a creation of bureaucracy.

They expect their own national governments to do the hard work of governing and to protect them from the worst of the European issues. They would be reluctant to give up their national sovereignty in the same manner as the states have in the US.

And if you go back to the founding of the US, you see that modern European attitudes are not at all different from what 18th-century Americans felt about Washington DC. Washington the man was more important than most now realize, as he gave the early government much of its legitimacy. The competing visions of Jefferson and Hamilton and the rest of the founding fathers led to some serious disagreements and public dissension. The election of 1800 was perhaps the most bitter and contentious one in US history, far nastier than today’s (“If Jefferson is elected all the churches will be shut down,” etc). And then there was that little dispute over states’ rights that came to a boil in 1860.

If politicians in 1792 had tried to sell voters on a full fiscal union as a reason to vote for the Constitution, we might still be debating the Articles of Confederation today.

And that is the crux of the problem that Europe. The costs of choosing either break-up or a fiscal union are so high and fraught with contention that to ask voters to choose with full knowledge of the costs would be to ask the question and not know the answer.

So why not choose fiscal union light? Rather than trying to reach the finish line in one huge leap, why not take a series of smaller steps? Let the pot heat slowly, rather than bringing it to a boil quickly. Like the proverbial frog, by the time European voters notice how hot it is, it will be too late to jump out.

But the hitch is, that might be the most costly route in the long run. It would mean bouncing from crisis to crisis, with each crisis costing more to resolve – but just not enough to make everyoone walk away. The longer the process is drawn out, the more expensive it will be.

We know about Spanish and Italian problems. What European leaders have not recognized (and indeed most of the world hasn’t, from what I see) is that France is the real problem. France is careening toward a dénouement of biblical proportions. Within a few years it will be just as problematic as Spain is today. France is in deep, deep foie gras.

Germany thinks it has an AAA debt partner for its guarantees of European debt in the EFSF, ESM, etc. It does today, but France will soon lose that AAA rating, absent significant changes that are not going to be forthcoming under Hollande and the Socialists. It could happen as early as September, although I doubt Moody’s or S&P will move before the German Constitutional Court ruling on the 12th – unless of course they really want to demonstrate their independence of thought from the political considerations of the moment!

And that ratings cut will just be the first of many. France is in the process of raising taxes on “les riches,” or those making over €1 million, to a nose-bleed 75%. Why stay in France when you can move, pay lower taxes, and visit when you want to? The new law will end up lowering, not raising tax collections, as has been shown by recent state tax hikes on the rich in the US. People vote with their feet.

In France it is not just the tax on the rich that is leading to trouble but so many other actions, like lowering the retirement age to 60, even though people are living longer and there are fewer people paying into the system as the nation ages. France has a near-term entitlements problem at least as severe as the US’s, but government spending is already at 55% of GDP.

By the time France becomes the clear problem, European voters will have committed so much to the process that to walk away will be far more costly than it would be today. Unless Merkel can somehow convince Hollande to really cut social spending dramatically in the coming years, the day of reckoning will arrive. And how has the deficit-cutting approach worked out for Spain, Greece, et al.? For that matter, Germany is in violation of the treaty deficit rules.

My guess: it will be Disaster C, which will mean a longer and more pronounced recession cum depression for much of Europe. And there could be mass public movements to leave the euro in any number of nations. While there is nowhere near a majority for that move in any country in any poll I have seen, it is a growing minority.

As part of this save-the-euro process, I fully expect that at some point there will be a mechanism that allows the ECB to monetize debt and buy peripheral bonds on a very large scale. We are talking multiple trillions of euros, as once you start that process you must continue it until the target country has gotten its deficit under control and is growing again. Whether it is the ESM becoming a bank or being allowed to issue bonds that the ECB can then use as collateral, or any of several schemes being proposed, the only real source of adequate firepower is the ECB. Sooner or later, the Germans will have to let the ECB off its leash, and that will not be good for the euro. And most definitely not when it is France with the problem.

The corollary to this view is that the euro problem will not go away for years. We will get euro fatigue, like Greek fatigue but writ larger. As in the days of my youth, this is going to be like a very long road trip across the country in a car with no air conditioning in the middle of summer, with three young kids and a cranky mother-in-law. Stay tuned.

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. Contact John at John@FrontlineThoughts.com.

Disclaimer

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions.

|

|

Free Festival of Traders Videos

Free Festival of Traders Videos