Navarro's Market Rap

We've got the flatsies in a market where there is enough uncertainty as to make me market neutral. My version of that is to be short QQQQ and long a few positions -- ASTM and TWP from last week, which had a very nice week, thank you very much. I pulled the plug on DHB on some negative executive team news and took a nice little gain on AMKR.

My suggestion for this week is to read Davio carefully and check out several of his charts of the week.

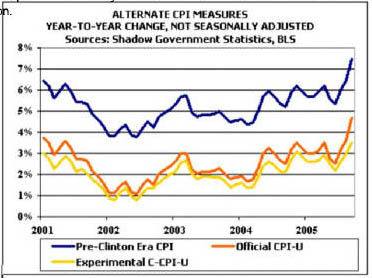

One chart shows that inflation is likely being understated by the gremlins in the bureaucracy that changed how to calculate inflation -- ergo the push on gold and the continued insistence of central banks around the globe to push up interest rates.

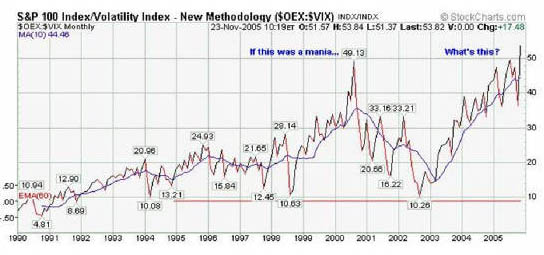

A second chart compares 2000 to now and suggests that manias come in pairs.

Keep your powder dry and your assets liquid.

P.S. The big market mover this week could be the CPI. It's all about the core now. Substantially above 2%, and the market tanks and conversely.

Hedging Your Bets With Matt Davio

Valuation is rarely a sufficient reason to be long or short the market. Absurdity is like infinity. Twice infinity is still infinity. Twice absurd is still absurd. Absurd valuations, whether high or low, can become even more absurd if the expectations of market participants become momentum-based. Momentum investors do not care about valuation; they buy what is going up, and sell what is going down.

You'll know a market top is probably coming when:

- The shorts already have been killed. You don't hear about them anymore. There is general embarrassment over investments in short-only funds.

- Long-only managers are getting butchered for conservatism. In early 2000, we saw many eminent value investors give up around the same time. Julian Robertson, George Vanderheiden, Robert Sanborn, Gary Brinson and Stanley Druckenmiller all stepped down shortly before the market top.

- Valuation-sensitive investors who aren't total-return driven because of a need to justify fees to outside investors accumulate cash. Warren Buffett is an example of this. When Buffett said that he "didn't get tech," he did not mean that he didn't understand technology; he just couldn't understand how technology companies would earn returns on equity justifying the capital employed on a sustainable basis.

- The recent past performance of growth managers tends to beat that of value managers. (I am using the terms growth and value in a classic sense here. Growth managers attempt to ascertain the future prospects of firms with little focus on valuation. Value managers attempt to calculate the value of a firm with less credit for future prospects.) In short, the future prospects of firms become the dominant means of setting market prices.

- Momentum strategies are self-reinforcing due to an abundance of momentum investors. Once momentum strategies become dominant in a market, the market behaves differently. Actual price volatility increases. Trends tend to maintain themselves over longer periods. Selloffs tend to be short and sharp.

- Markets driven by momentum favor inexperienced investors. My favorite way that this plays out is on CNBC. I gauge the age, experience and reasoning of the pundits. Near market tops, the pundits tend to be younger, newer and less rigorous. Experienced investors tend to have a greater regard for risk control, and believe in mean-reversion to a degree. Inexperienced investors tend to follow trends. They like to buy stocks that look like they are succeeding and sell those that look like they are failing.

- Defined benefit pension plans tend to be net sellers of stock. This happens as they rebalance their funds to their target weights.

Chart of the Week 1

Notice how the OEX and VIX is higher than we saw in the 2000 bubble. Is there a bubble now? You decide.

Chart of the Week 2

Yesterday I received the above illustration from Gillespie Research. The blue line shows how CPI would be calculated by measures used prior to the Clinton Administration. It suggests that contrary to the deflation dogmatists, inflation is alive and well, which may well help explain a bull market in gold. Perhaps this is also why most of the central banks of the world are raising rates to fight inflation.

Peter Navarro is a business professor at the University of California-Irvine, and can be contacted at pn@peternavarro.com. Matt Davio is a managing partner at the hedge fund, Red Rock Capital Fund, and be contacted for hedge fund services at redrock@peternavarro.com.

DISCLAIMER: This newsletter is written for educational purposes only. By no means do any of its contents recommend, advocate or urge the buying, selling, or holding of any financial instrument whatsoever. Trading and investing involves high levels of risk. The authors express personal opinions and will not assume any responsibility whatsoever for the actions of the reader. The authors may or may not have positions in the financial instruments discussed in this newsletter. Future results can be dramatically different from the opinions expressed herein. Past performance does not guarantee future performance.

Free Festival of Traders Videos

Free Festival of Traders Videos